Real Estate News

Real Estate News

Published Date: 2025-10-23

Exclusive Offer!

Do you want to be in the know on housing issues and linked to other providers asking relevant questions about your industry?

Join Corporate Housing &...

read more

Real Estate News

Real Estate News

Published Date: 2019-04-10

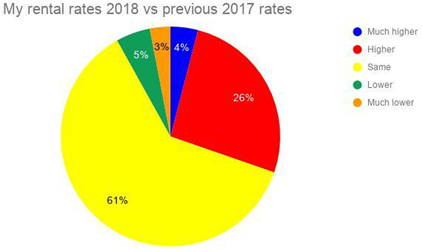

Variance: Changes in Rental

Rates

We asked respondents to evaluate their current rental rates compared to the previous year for the exact same rental property.

Annual...

read more

Real Estate News

Real Estate News

Published Date: 2019-04-03

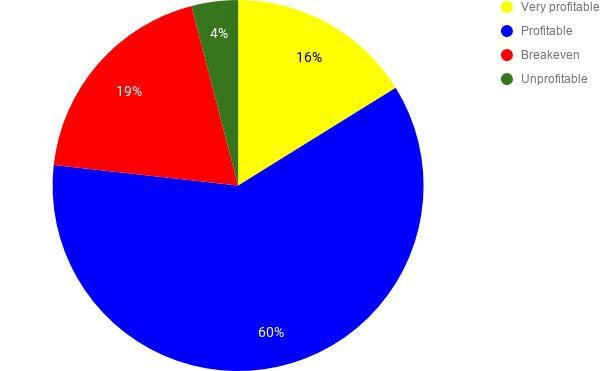

Outlook & Profitability

2018 is the highest year with ?96% of participants stating their property was either profitable (76%) or breakeven (19%)?. Only 4% of owners said their property was...

read more

Real Estate News

Real Estate News

Published Date: 2019-03-27

Property Locations

We received hundreds of survey responses from property owners and real estate managers across the United States.

Similar to last year, the ?top U.S. states for responses?...

read more

Real Estate News

Real Estate News

Published Date: 2018-07-17

Profitability

Great news for Corporate Housing?, the fifth year in a row, more than 9 out of 10 respondents ?report their properties are profitable or break-even.

Over the last few years we have...

read more

Real Estate News

Real Estate News

Published Date: 2018-07-12

The results are in, so let’s dig deeper. Each week CHBO will analyze data from the annual corporate housing report and open a discussion. Please provide feedback with your experiences in 2017. This...

read more

Real Estate News

Real Estate News

Published Date: 2015-12-15

With so many corporate employers in the region, Albuquerque is a growing hotspot for business travelers. The need for Albuquerque furnished housing has been increasing over time, and if you are...

read more

Real Estate News

Real Estate News

Published Date: 2015-11-10

Are you headed to Colorado Springs for an extended stay? Whether you’re planning on relocating permanently to this idyllic area of one of the most beautiful states in the country or you just need a...

read more

Real Estate News

Real Estate News

Published Date: 2014-12-30

City Spotlight: Buenos Aires

It might be the capital and largest city of Argentina, but there’s a lot that makes Buenos Aires stand out beyond that. It’s an incredibly beautiful city, bounded by...

read more